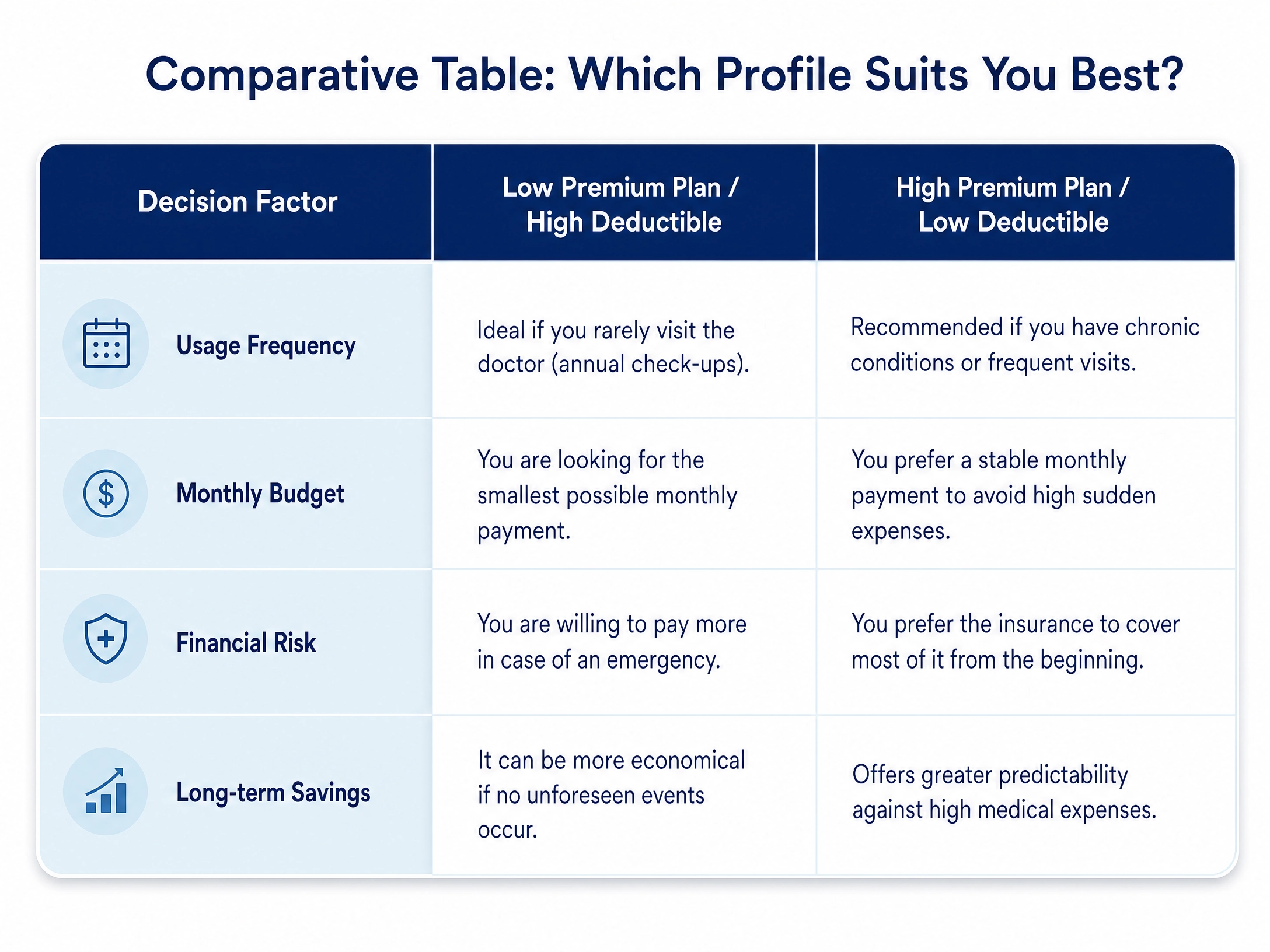

Choosing between a low monthly premium or a reduced deductible depends on how frequently you use medical services. Generally, those who visit the doctor rarely prefer low premiums, while those who require constant medical attention usually benefit from lower deductibles.

In the complex world of health insurance in the United States, making the right decision can seem like an overwhelming challenge. At AV Prada, our mission is to simplify this process so that you and your family are protected without compromising your financial stability. The key to saving is not always in the cheapest plan, but in the one that best adapts to your lifestyle.

What is the premium and how does it affect your monthly budget?

The premium is the fixed payment you make month after month to keep your health coverage active, regardless of whether you use medical services or not. It is, in essence, the cost of your peace of mind.

Low premiums: These are usually associated with plans where the user assumes more out-of-pocket costs at the time of receiving care.

High premiums: These generally offer broader coverage from the very first dollar, reducing your unexpected expenses at the clinic or hospital.

What is the deductible and why is it vital to understand it?

The deductible is the amount of money that the insured must pay for covered health services before the insurance company begins to pay. It is a determining factor in the final cost of any medical procedure.

"Understanding your deductible is the difference between a financial surprise and smart planning."

Which one should I choose if I want to save on my medical expenses this year?

The answer is not universal, as each case is personalized and subject to evaluation. However, we can consider these general trends:

Myths vs. Realities About Healthcare Costs

Myth: The plan with the lowest premium is always the one that saves me the most money.

Reality: If you suffer an unexpected accident or illness, a plan with a very high deductible could end up being much more expensive by the end of the year.

Myth: Once the deductible is paid, everything is free.

Reality: Generally, after the deductible is met, coinsurance or copays come into play until you reach the out-of-pocket maximum.

How do my location and profile influence this decision?

It is important to remember that health insurance is state-specific by nature. If you decide to move to another state, it is essential that you contact your AV Prada agent, as provider networks and regulations can vary significantly. Additionally, remember that most plans limit their coverage to emergencies when you travel outside your insurance company's network.

Frequently Asked Questions

1. Can I change my deductible at any time of the year?

Generally, changes to your plan structure can only be made during the Open Enrollment Period, or if you qualify for a Special Enrollment Period due to qualifying life events, such as marriage or the birth of a child.

2. What is the out-of-pocket maximum?

It is the maximum limit you will pay for covered services in a plan year. After reaching this amount, the insurance company pays 100% of the covered services. It is your greatest protection against financial catastrophes.

3. How do I know which plan suits me best?

The best way to know is through a personalized consultation. Factors such as your age, medical history, and family composition directly influence the final recommendation.

Take Control of Your Financial Health Today

Don't leave your well-being to chance. At AV Prada, we are ready to analyze your case individually and help you find that perfect balance between premium and deductible.

Want to know what the best option is for you this 2026? Click here to receive a free, personalized consultation