Understanding the premium, deductible, and copayment is crucial for managing health costs in the United States. These terms define how medical expenses are shared between you and the insurer, offering financial clarity according to the plan you choose.

What do my health insurance key terms really mean?

Navigating the healthcare system can seem like a maze of complex terms. At AV Prada, our mission is to simplify these concepts so you can protect your family with total confidence, transforming technical information into clear tools for your decision-making.

What is the Premium?

The premium is the regular cost you pay (usually each month) to keep your health insurance coverage active. This payment is independent of whether or not you use medical services. It is, in essence, the price for having your policy in effect.

What is the Deductible?

The deductible is the amount of money that you generally must pay out of pocket for covered health services before your insurance plan begins to cover its part. It is important to understand that the deductible is commonly applied to procedures or services that are subject to coinsurance. The amount of your deductible depends primarily on the type of insurance plan you choose.

What is Coinsurance?

Coinsurance is the percentage of the costs of a covered medical service that you are responsible for paying after you have reached your deductible. For example, if your insurance covers 80% of a service, you would assume the remaining 20%. This percentage generally applies to medical exams, procedures, and emergency services.

What is the Copayment (Copay)?

The copayment is a fixed amount of money that you pay directly at the time you receive a medical service, such as a doctor's visit or the purchase of a prescription drug. Unlike the deductible, the copayment is a fixed value that does not vary and is not subject to whether you have met your deductible. This means that even if you still have an outstanding deductible, the copayments remain.

What is the Out-of-Pocket Maximum?

The out-of-pocket maximum is the highest total amount you would pay for covered health services in a year. Once you reach this limit, your insurance plan will cover 100% of eligible costs for the rest of the year, protecting you from catastrophic medical expenses.

How do government subsidies influence these costs?

Government assistance, such as the tax credit (Marketplace subsidy), applies specifically to your plan's monthly premium. It is crucial to understand that this subsidy does not directly modify your policy's benefits, such as copayments, deductibles, or coinsurance. These values depend on the type of plan you select (e.g., Bronze, Silver, Gold, etc.), not the amount of the subsidy.

It is important to highlight that government assistance does not always reduce the deductible. Only in some specific cases and with certain plans, depending on your income, could there be a reduction in cost-sharing. Therefore, personalized advice is fundamental to understanding how these factors apply to your situation.

How to choose the right health insurance plan for you?

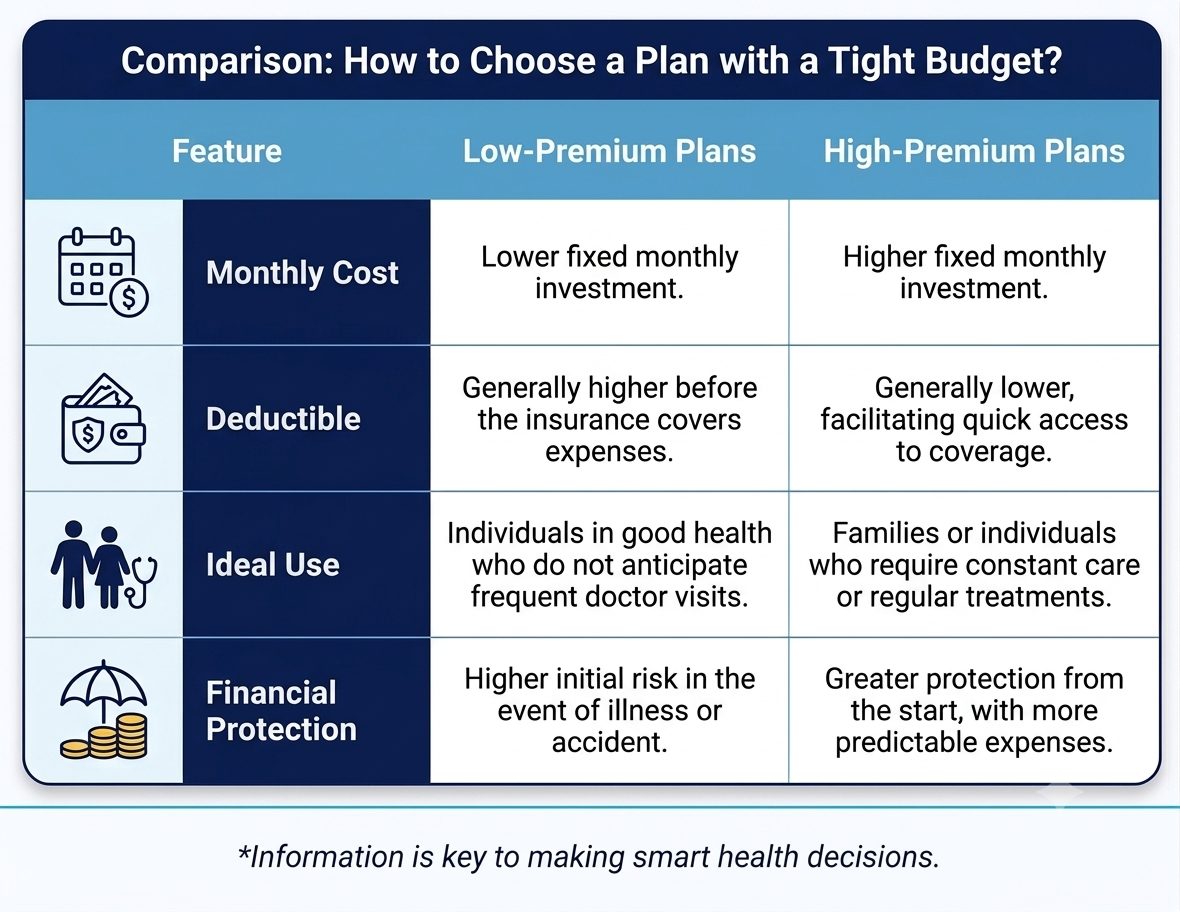

There is no "one-size-fits-all" plan that is perfect for everyone. The ideal choice depends on your individual medical needs and those of your household. Generally, there is an inverse relationship between what you pay each month (premium) and what you pay when you use the services (deductible, copayment, coinsurance).

Qualitative Comparison: Types of Plans and their Characteristics

Myths vs. Realities about health insurance costs

Myth: "If I have insurance, I don't have to pay anything when going to the doctor."

Reality: Most plans require you to share costs through copayments, deductibles, or coinsurance until you reach your annual out-of-pocket maximum. Your insurance begins to cover most expenses once you fulfill these responsibilities.

Myth: "The cheapest plan (with a low premium) is always the best for saving money."

Reality: A plan with a low monthly premium can result in being more expensive in the long term if you need frequent medical attention or if an emergency occurs, as the deductible and coinsurance could be very high. It is fundamental to consider the total cost, not just the premium.

Myth: "Government subsidies always lower my deductible and copayments."

Reality: Marketplace subsidies (tax credits) are applied primarily to the monthly premium. Although in some cases and depending on your income, you might qualify for reductions in cost-sharing (deductibles and copayments), this is not a general rule and depends on your profile and the chosen plan.

Frequently Asked Questions

What factors influence the cost of my deductible?

The amount of your deductible varies according to the type of insurance plan you choose, the specific policy benefits, and whether you qualify for federal aid programs that can reduce your cost-sharing, which depends on your income and family situation.

When do I stop paying for covered services?

You stop paying most costs when you reach your annual out-of-pocket maximum. Once this limit is reached, your health insurance will cover 100% of eligible expenses for the rest of the year, provided that you use providers within your plan's network and the services are medically necessary.

Do I have to pay the deductible before seeing my primary care doctor?

Many plans offer certain preventive services or primary care visits with only a copayment, even before you have met your deductible. However, this is subject to the specific terms of your current plan, and it is important to review them carefully.

Find the perfect balance for your pocket and your health

At AV Prada, we know that every situation is unique. Do not allow confusing terms to prevent you from making the best decisions for your health and your finances. Let us help you decipher what the ideal combination of premium, deductible, copayment, and coinsurance is for your particular situation.

Ready to understand your coverage without complications and protect your family?

Request your personalized consultation today and take control of your financial health.