Many people avoid purchasing health insurance due to mistaken beliefs about its cost and complexity. This article debunks the most common myths, demonstrating that affordable options adapted to various needs exist, thereby facilitating the protection of your well-being and that of your family in the United States.

Why is it crucial to understand health insurance in the United States?

In the United States, the healthcare system can seem complex, and misinformation often leads to wrong decisions. Understanding how health insurance works is fundamental to protecting your health and your finances. At AV Prada, our mission is to guide you so you can find the ideal coverage, debunking the preconceived ideas that prevent you from taking the step toward comprehensive protection.

Myths vs. Realities: Clearing the path toward your protection

Is health insurance really unattainable?

Myth 1: "Health insurance is too expensive and I cannot pay for it."

Reality: This is one of the biggest concerns, but it is often based on incomplete information. There are various health insurance options, including Health Insurance Marketplace plans (known as Obamacare or ACA), Medicare for people over 65 or with certain disabilities, and private insurance. Many individuals and families generally qualify for federal subsidies that can significantly reduce the cost of monthly premiums, making coverage much more accessible than imagined. The key lies in exploring all alternatives and understanding the factors that influence the cost, such as your age, location, income, and the type of plan. Instead of focusing on a fixed cost, it is important to understand that the final price is personalized and can vary considerably.

Is health insurance only for emergencies?

Myth 2: "I only need insurance if I get seriously ill."

Reality: Health insurance is not just for emergencies. It also covers preventive care, such as annual checkups, vaccines, and screening exams, which are vital to maintaining good health and detecting problems on time. Furthermore, insurance protects you from the high costs of medical care in general, from doctor visits and prescription medications to hospitalizations and surgeries. Without coverage, an unexpected illness or accident could generate overwhelming medical debts that affect your financial stability.

Is insurance terminology too complex to understand?

Myth 3: "It is very complicated to understand the terms and conditions of an insurance policy."

Reality: It is true that insurance terminology can be confusing at first. Concepts such as deductible, copayment, coinsurance, and out-of-pocket maximum are fundamental. However, you do not have to decipher them alone. At AV Prada, we are dedicated to explaining these terms clearly and simply, making sure you understand exactly what your plan covers and what your financial responsibilities are. Our goal is to empower you with knowledge so you can make the best decision.

Understanding the key terms:

Deductible: It is the amount that the insured assumes before the insurance company begins to cover the expenses of certain services. Generally, the deductible applies to procedures or services that are subject to coinsurance. Once you reach your deductible, the insurance starts covering a part or the entirety of your expenses, according to the terms of your plan.

Coinsurance: Corresponds to the percentage that the client is responsible for paying after having reached the deductible. For example, if the insurance covers 80% of the service, the client would assume the remaining 20%. Generally, this applies to medical exams, procedures, and emergency services.

Copayment: It is a fixed value that does not vary and is not subject to the deductible. This means that, even if you still have a pending deductible to exhaust, the fixed values of the copayments remain for specific services, such as visits to a general doctor or specialist.

Out-of-Pocket Maximum: It is the maximum amount of money that you will have to pay on your own for covered services in a policy year. Once you reach this limit, your health plan pays 100% of the costs of covered services for the rest of the year.

Do preexisting conditions prevent obtaining coverage?

Myth 4: "If I have a preexisting condition, I will not be able to obtain coverage."

Reality: Thanks to the Affordable Care Act (ACA), insurance companies cannot deny you coverage or charge you more because of a preexisting health condition in Health Insurance Marketplace plans. This has been a fundamental change that guarantees everyone has access to necessary medical care. While short-term insurance may have limitations in this aspect, Marketplace plans are designed to protect you regardless of your medical history.

Do all health insurances offer the same?

Myth 5: "All health insurances are the same."

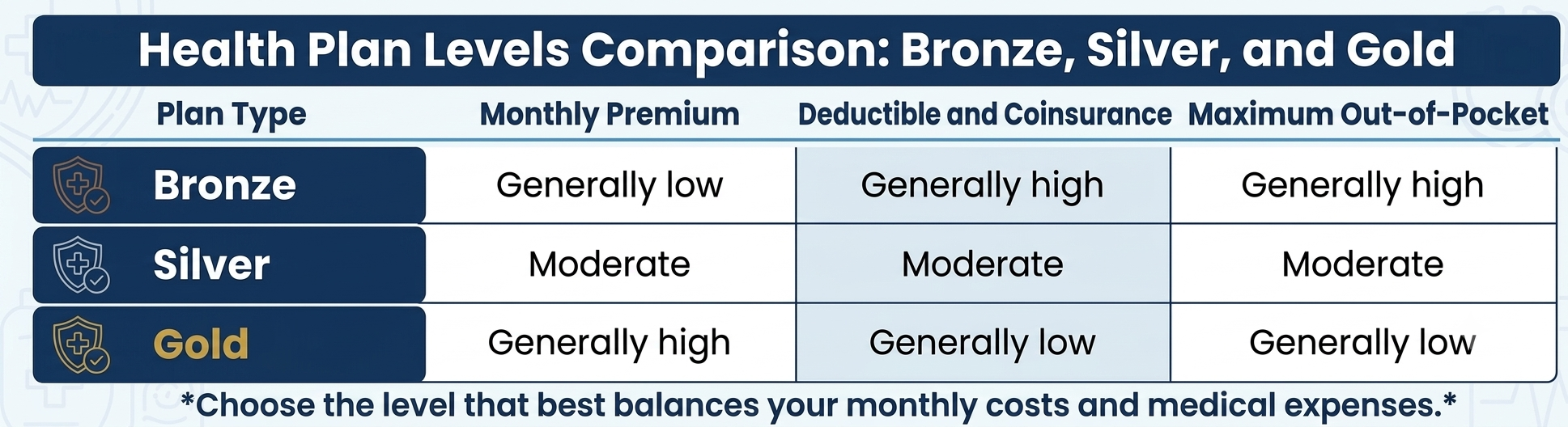

Reality: Health insurances vary enormously in terms of coverage, provider network, costs, and additional benefits. Some plans focus on low monthly costs with higher deductibles (such as Bronze plans), while others offer higher premiums in exchange for lower out-of-pocket expenses (such as Gold plans). Choosing the right plan depends on your profile, your health needs, your budget, and your personal preferences. Personalized advice is key to finding the one that best adapts to you.

Qualitative Comparison of Plan Types (Example):

Additional Considerations for Your Coverage

How do federal subsidies affect my deductible or copayment?

The tax credit (Marketplace subsidy) applies solely to the monthly premium of the plan and does not modify the benefits of the policy, such as copayments, deductibles, or coinsurance. These values depend on the type of plan you choose (Bronze, Silver, Gold, etc.), not on the amount of the subsidy. Government help does not always lower the deductible, only in some specific cases and with certain plans, depending on the person's income.

What should I consider if I move or travel?

Health insurance in the United States has a state-specific nature. If you move to another state, it is crucial that you get in touch with your AV Prada insurance agent, since your current plan will probably not cover you in your new location. For travel, coverage may be limited to emergencies and to your company's network of providers, especially outside the state or the country. It is advisable to research travel insurance options or speak with your agent to ensure your protection.

Protect what matters most: Your health and that of your family

At AV Prada, we understand that health is your greatest asset. Do not let myths prevent you from obtaining the protection you deserve. We are here to clear up your doubts, simplify the process, and help you find the ideal health insurance that fits your needs and budget. Our experience and commitment are at your service so you can make informed decisions and protect your family.

Do not wait any longer to ensure your peace of mind!

Write to us today for a personalized and free consultation. Let us be your ally in the protection of your well-being.