Why does your family health insurance need a boost?

At AV Prada, we know that even the healthiest children are prone to the unexpected: a fall at the park or an emergency visit due to a high fever. Even if you have health insurance, out-of-pocket expenses can be overwhelming.

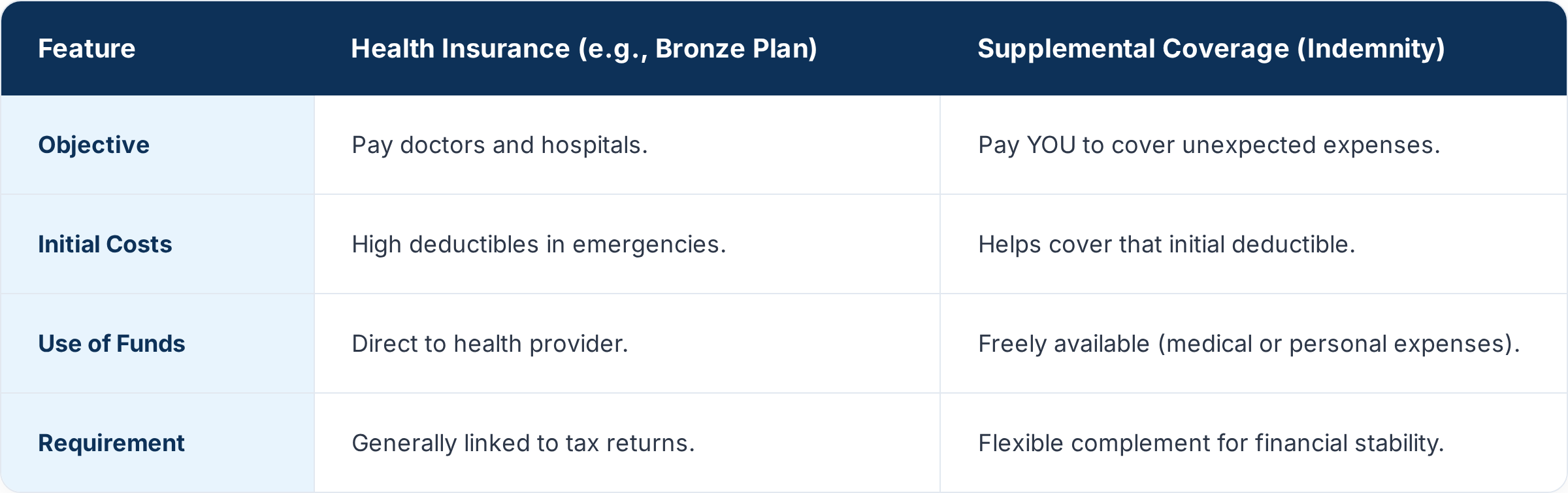

Most families opt for Bronze Plans due to their lower monthly premiums. These plans typically cover primary care visits with fixed copays, but in the event of a hospitalization or emergency, the client must cover high deductibles and coinsurance before the insurance pays the bulk of the expenses. This is where supplemental coverage steps in to protect your wallet.

The role of Hospital Indemnity in childhood accidents

Unlike traditional health insurance, Hospital Indemnity pays you directly if a family member is admitted.

Cash in hand: You receive a set amount to cover the primary insurance deductible or household expenses.

No usage restrictions: You can use the money for whatever you need while focusing on your child’s recovery.

Focus on accidents: It is ideal for families with active children, as they are the ones who most frequently face unexpected hospitalizations.

Myths vs. Realities

Myth: "Dental and vision care are mandatory and included in all plans for minors."

Reality: This only happens in specific plans; it is not a general rule. It is vital to verify the benefits of your particular policy.

Myth: "I need a 'Qualifying Life Event' to add my children."

Reality: In most states, a life change is not required to add your children to the coverage.

Eligibility Requirements and Taxes

It is fundamental to understand that the protection of your dependents is linked to your tax situation:

Family Nucleus: Anyone you wish to include in your policy must be part of the family nucleus you declare on your taxes.

The 26-Year Rule: Children can remain on the plan until the end of the month they turn 26 or the end of the year, but this will depend on whether you still claim them as dependents on your taxes and on state laws.

Comparison: Health Insurance vs. Hospital Indemnity

Can I get a supplemental policy if I already have health insurance?

Absolutely! In fact, it is highly recommended to prevent an emergency from draining your savings due to the primary plan's deductibles.

What requirements must I meet to add a dependent?

You must meet the plan's eligibility criteria and ensure the dependent is part of your tax return.

Does hospital indemnity cover any hospital?

Generally, these policies pay for the hospitalization event regardless of the network, but it is always best to review the terms of your contract with an AV Prada advisor.

Your peace of mind begins with an informed decision

Don’t wait for an accident to happen to realize the gaps in your coverage. At AV Prada, our mission is to ensure that, in an emergency, your only concern is your child’s well-being, not your bank account balance.

Want to protect your savings and your family today?

Schedule a personalized consultation and discover how supplemental coverage can give you the peace of mind you need.